We close the gap between how your business actually works and what the institution needs to see to support it.

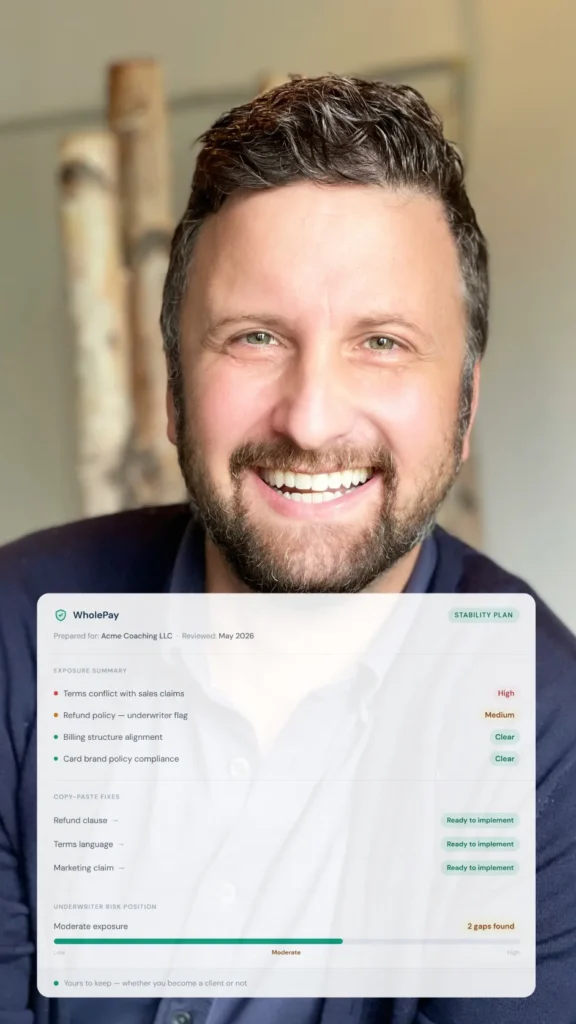

We align your business with bank and card brand policy before you apply. Every WholePay client goes through a forensic review. We look at their offers, terms, refund language, marketing claims, and pricing structure. We find the gaps. We close them. By the time the application reaches an underwriter, the bank is reviewing a business that is already aligned.

ScaleSafe builds your defense record into every transaction. Consent records, communication logs, delivery confirmations are captured automatically as you work. When a chargeback comes in, ScaleSafe pulls that data and generates a complete evidence package. You are not scrambling for evidence. The system builds it for you.

You see every dollar. Every month. Transparent, disclosed, fit-based pricing. No bundled rates. No tiered markups. No hidden fees.

You have a team in your corner. Not a support ticket. Not a chatbot. People who understand how underwriting works, what card brand policy actually says, and who will pick up the phone and advocate for your account when it matters.