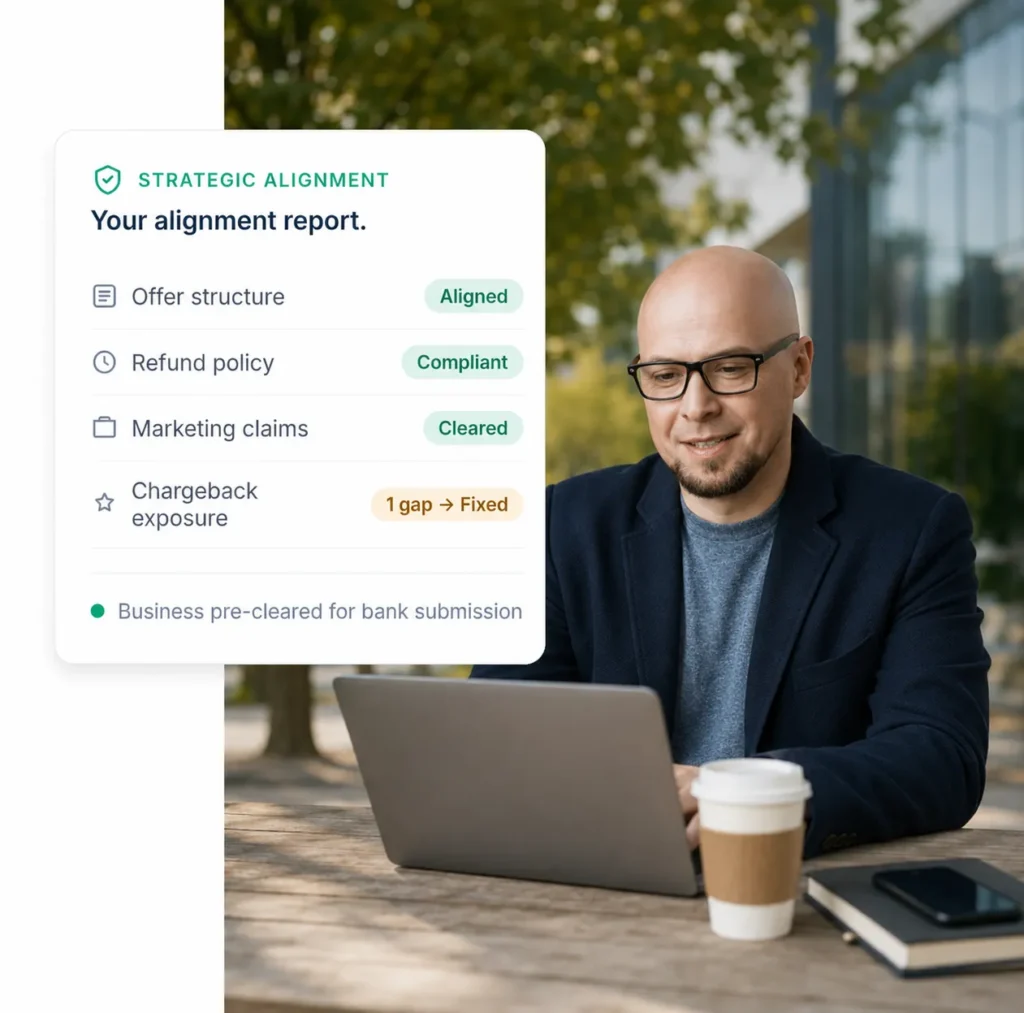

We identify language in your sales page and checkout flows that triggers risk flags: income claims, guaranteed results, vague deliverables. Then we fix it.

The first documents an underwriter reads. They need to be clear, compliant, and aligned with what you actually sell and how you deliver.

How you charge relative to how you deliver. We make sure your billing structure matches your fulfillment model in a way the bank can approve.

What appears on your client's credit card statement. If it does not match your business name or website, confused clients file chargebacks.

Card brand policy has specific rules about what you can say when selling high-ticket services. Having your marketing reviewed and approved closes one of the biggest alignment gaps.

If dispute activity is trending toward thresholds, we identify the root cause and help you course-correct before it becomes an account-level problem.

Most processors skip this entirely. They approve you based on a basic application and move on. When something goes wrong, the burden falls on you.

We do the work upfront. By the time your application reaches a bank, the underwriting team sees a business that is already aligned.

Visa and Mastercard monitor dispute ratios across every merchant account. When ratios climb, the consequences escalate: per-dispute fees (currently $8 per dispute under Visa’s VAMP program), mandatory reserves on your account, enrollment in formal monitoring programs with additional fines, and in serious cases, account termination or placement on the MATCH list.

These thresholds are also getting stricter. Visa’s VAMP merchant threshold drops from 2.2% to 1.5% for North America in April 2026, and acquirer thresholds are tightening alongside them. That means processors will be watching their merchant portfolios more closely than ever, and the margin for error is shrinking.

Your processor also sets their own internal limits, often stricter than the card brands require, to protect their portfolio. High-ticket operators are uniquely exposed because dispute ratios are count-based. When you process fewer, larger transactions, each individual dispute has an outsized impact on your ratio. A business processing 200 transactions a month has almost no margin for error under the current VAMP thresholds.

Every merchant account has expected volume parameters set during onboarding. Those parameters are based on your application data, not on your growth plan. When a launch, a new offer, or a seasonal spike pushes you outside those parameters, automated systems flag the activity. Deposits get held. Processing can freeze. The system cannot tell the difference between a great month and suspicious activity unless someone has coordinated the volume in advance.

Card brand policy has specific rules about income claims, guaranteed results, and how you describe outcomes. Most high-ticket operators have never had their marketing reviewed by an underwriter who understands their model. That review closes one of the biggest alignment gaps in the industry, and it is one of the first things we address in the Stability Plan.

If your refund policy conflicts with what the card brand considers reasonable for your transaction type, the bank sides with the cardholder automatically. But refund policy is also strategic. How it is structured, when it is presented, how it is acknowledged, and whether it aligns with your billing and delivery model all affect how a bank evaluates a dispute. A refund policy that protects you legally but was never shown to the client at the right moment is a liability, not a defense.